The days when customers had to mail checks to businesses and wait weeks for the transaction to post are long gone. In the modern world, businesses can accept electronic payments from customers anywhere in the world, and some transactions can be processed in the blink of an eye. The development of new and improved payment technologies has revolutionized the way companies do business and created a more efficient, effective, and secure payment process for consumers.

From online payment gateways to electronic checks to real-time networks, the landscape of payment processing solutions is nuanced and complex. Small and medium-sized businesses (SMBs) have many options when it comes to selecting the payment technologies that work best for their size, structure, and purpose. Before leaders of SMBs can decide whether one, some, or all of these technologies are appropriate for their needs, it's important to look closely at what sets them apart and what specific benefits they offer.

Safely processing card-not-present transactions

A card-not-present (CNP) transaction is a remote payment where a customer does not swipe, tap, or insert their debit or credit card at a payment terminal. In some cases, the customer is present for the transaction but doesn't have their physical card on hand. In others, the customer and card are both in a different location from the business. In either case, these types of transactions are vital to SMBs that want to offer the highest level of convenience and flexibility to consumers.

Types of card-not-present transactions

The popularity of eCommerce has made CNP payments more important than ever, but they have long played a role in payment processing. In the past, when customers selected items they wanted to purchase from a catalog, they could make CNP payments by mailing in order forms or calling the sales line.

Phone and mail CNP transactions aren't as popular as they once were, but they remain a go-to method for customers who are unable or prefer not to pay their bills or make purchases online. Today's CNP transaction types have expanded to include:

- Online orders: Customers use their cards to purchase items through a business website or app. Some purchases are completed entirely online and items are shipped, while other businesses accept payment online for items that customers will pick up in person at a later date or time.

- Telephone purchases: Businesses can accept payments over the phone, allowing customers to complete their transactions no matter their current location. Organizations often use telephone numbers to help confirm a customer's identity and reduce the risk of fraud.

- Mail orders: To complete a purchase by mail, customers submit a paper with their credit card information to a business. The customer's signature may help verify the authenticity of the transaction.

- Card-on-file payments: When customers make frequent purchases or receive recurring services, a card-on-file payment allows the business to process payments without repeatedly collecting the same payment information. Customers must authorize businesses to use their cards for future purchases.

- Digital wallets: Payments from digital wallets make it possible for customers to complete CNP transactions in brick-and-mortar locations. Businesses can use contactless payment solutions, such as a tap-to-pay terminal, to accept payments from smartphones and wearable devices equipped with digital wallet software or apps.

Businesses aren't limited to accepting a single CNP type. Rather, SMBs can choose to accept all types of CNP payments using different POS technology, software, and tools.

What SMBs need to process card-not-present transactions

The method that an SMB uses to process a CNP transaction depends on the specific type of payment. Generally speaking, however, the steps involve obtaining detailed financial information from the customer, such as:

- Full legal name

- Billing and shipping addresses

- Phone number

- Card number

- Card expiration date

- Card security code

SMBs may also need access to special equipment or software to complete these transactions. For example, many organizations use virtual terminals to accept CNP payments over the phone, while eCommerce stores rely on payment gateways to complete online transactions.

Concerns about card-not-present transactions

Although CNP transactions offer a high level of convenience to customers and businesses, they also present problems that generally don't exist with card-present payments. The most significant issue is rampant fraud, which occurs much more frequently with CNPs than when customers complete in-person purchases with their physical cards.

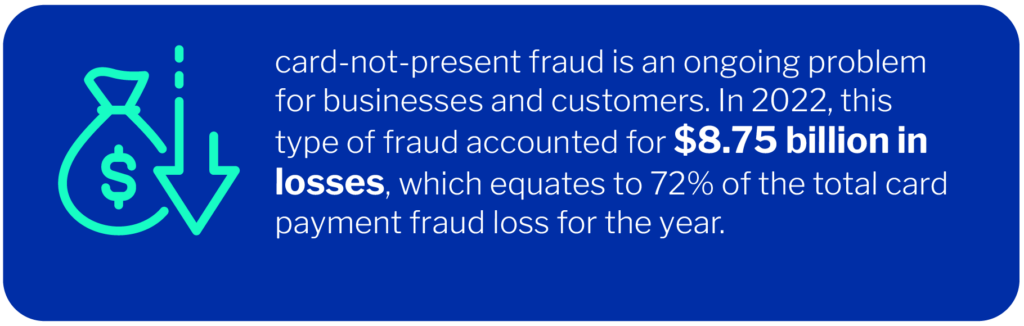

A report from Insider Intelligence indicates that losses from CNP fraud in the United States reached $8.75 billion in 2022, and the number is projected to grow to $9.49 billion in 2023. This growth parallels that of eCommerce sales, but the fact that CNP fraud accounts for more than 70% of all credit card fraud is cause for concern.

As a result of these problems, businesses generally pay higher merchant fees for CNP transactions. They also run the risk of paying expensive chargeback fees or losing customers because of false declines.

Security improvements are the key to reducing fraud and giving payment processing providers greater confidence in the validity of CNP transactions. For businesses in eCommerce, tokenization and encryption are essential, and many companies are moving toward two-factor authentication for an additional layer of security. Unfortunately, these tools aren't viable for mail order and virtual terminal payments, and they must instead rely on recorded audio authorizations and signatures for identity verification.

Simplifying electronic payments with payment gateway integrations

SMBs that operate partially or fully online can't function properly without an effective payment gateway connected to their POS system. In addition to selecting the right gateway provider, businesses must also decide which type of payment gateway integration they prefer.

The importance of payment gateway integrations

In 2021, the global online shopping cart abandonment rate was nearly 70%, reflecting the challenges that online SMBs face when attempting to convert site visitors into paying customers. Some customers abandon their carts because they rethink the purchase, but many are deterred by issues with the checkout process. A 2019 survey found that 20% of respondents abandoned their shopping carts because they couldn't use their preferred payment method. Other customers gave up on their shopping because they found the checkout process overly complicated or lengthy. Both of these problems can be remedied with the right payment gateway integration.

The growing need for effective digital payment services has led to explosive growth in the payment gateway industry. According to Future Market Insights, the online payment gateway market is projected to reach $117.5 billion in 2023 and rise to $293.9 billion by 2033.

Types of integrations

To create a seamless checkout experience and maximize efficiency, SMBs should select a payment gateway integration that aligns with their existing technology and business management software. Some integrations are relatively hands-off and require very little effort on the part of the business owner, while others offer a higher level of control and responsibility.

Hosted payment gateways

SMBs that don't want to worry about regulatory compliance and data storage may find the most benefit from a hosted payment gateway, which directs customers away from the business's primary website to a payment service provider page. Once there, the customer can enter their payment information and complete the transaction, before being sent back to the business website or app.

Some banks also offer this service, allowing SMBs to direct customers to a payment page within the bank's website. However, these pages often don't allow customers to set up recurring payments, subscription services, or returns.

Hosted gateways are appealing because they require very little setup on the part of the business and offload maintenance and Payment Card Industry Data Security Standard (PCI DSS) compliance to a third party. Sensitive payment information is also held on the payment gateway provider's site, mitigating the business's liability should a data breach occur. As such, hosted gateways are extremely secure. However, because the payment gateway is hosted on a separate site, businesses have no control over the structure or appearance of the payment page, which could lead to frustrating or disjointed customer experiences.

Direct post payment gateways

One of the downsides of a hosted payment gateway is the fact that the customer is redirected to a new site. A direct post payment gateway is a potential solution to this issue because it offers similar benefits while also allowing customers to remain within the business's app or website while completing their transactions.

When an SMB uses a direct post gateway, the payment is completed through a third-party provider. However, unlike a hosted gateway, the customer enters their payment information on the business page or app, and it’s then transmitted to the payment gateway server. The gateway provider is responsible for PCI DSS compliance and storing sensitive data, alleviating the burden of security for the SMB owner. This fast and easy option is a good alternative to a hosted gateway, but it still offers limited customization in the checkout process.

Self-hosted white-label payment gateways

SMBs can achieve greater control over their customer checkout experience with prebuilt self-hosted payment gateways. Because they're integrated directly into the business website with an Application Programming Interface (API), these gateways offer a faster checkout process that's free of redirects.

To ensure that every customer's data is protected, SMBs with self-hosted white-label gateways must use strong security measures and achieve PCI DSS compliance. Additionally, businesses with these gateways don't have access to a technical support team to help maintain the gateway infrastructure and address security concerns.

Self-hosted custom payment gateways

When a business owner wants complete control over the checkout process, a custom payment gateway is likely the answer. From accepted payment methods to the checkout flow, SMBs can build payment gateways that meet all of their needs and preferences.

This level of customization brings with it a higher cost and level of responsibility. Building a payment gateway from scratch is time-consuming and expensive, and it may not be worthwhile for a small business. Furthermore, because there’s no third-party provider involved, the business assumes full responsibility for PCI DSS compliance and infrastructure upkeep.

The cost of payment gateway integration

The exact price of integrating a payment gateway into an SMB's website or app differs based on the gateway provider and the integration type. Some providers charge setup fees, while others allow businesses to integrate gateways for free. Business owners that opt to develop a custom payment gateway will spend considerably more than those who use white label or hosted gateways.

Regardless of the integration type, businesses can expect to pay merchant processing fees. Some providers offer fixed monthly rates, and others charge a fee for each transaction.

Replacing paper checks with electronic payments

Paper checks and cash were once the primary payment method for consumers, but they've gradually been replaced by digital and electronic payments. A 2023 survey by Yahoo found that 45% of Americans hadn't used a paper check in the past year, and only 5% wrote more than one check per month. As a result, SMBs have employed other payment technologies, namely electronic checks and the Automated Clearing House (ACH) network, so that customers can make payments from their bank accounts without using physical checks.

Electronic check processing

Also known as eChecks, electronic checks are a faster, more convenient version of traditional paper checks. They enable customers to pay for products or services online as opposed to in person, over the phone, or through the mail, accelerating the speed of payment processing for businesses.

In 2003, the United States government passed the Check Clearing for the 21st Century Act, which established a legal foundation for electronic check processing. Since then, eChecks have become one of the most popular payment methods for businesses. To process them, businesses only need to collect basic information from the customer, including:

- Name on the account

- Bank routing number

- Account number

- Written or recorded audio authorization

After entering this information into their system, businesses can initiate a transaction that withdraws funds from the customer's bank account and transfers it directly to the merchant's account via the ACH network.

SMBs can benefit from electronic checks in a variety of ways, such as:

- Reduced costs: The processing fees for eChecks are typically lower than those for credit card payments. Additionally, the labor and materials costs for paper checks are generally much higher than those for eChecks.

- Security: Encryption and authentication make eChecks much more secure than paper checks. They also eliminate the potential for check fraud resulting from mail theft, which has surged in the past three years.

- Minimal waste: Traditional checks result in excessive paper waste, not only from the checks themselves but also from envelopes and packaging used during mailing. Accepting eChecks is an easy way to reduce a business's environmental impact.

- Faster processing: Payments from eChecks are generally processed in batches, so businesses often have to wait a few days for the money to be released. While they don't process as quickly as credit card or digital wallet payments, eChecks can be significantly faster than paper checks, which might spend days or weeks in the mail.

Payments made via eCheck are generally best suited to SMBs that sell high-cost items or charge monthly fees. For example, customers might use eChecks to pay for their rent, car, or gym membership.

ACH payments

The Automated Clearing House was first established in 1972 as a means of processing and routing electronic payments. It's critical to financial institutions and businesses throughout the United States because it's a secure and safe way to transfer money.

In addition to consumer purchases, the ACH network is also useful for government payments and business-to-business transactions, such as when an SMB pays a vendor or supplier. The ACH enables both credits, in which the customer initiates a payment to a business or organization, and debits or withdrawals that are initiated by merchants.

ACH payments are usually straightforward. As with eChecks, a business collects a customer's financial information, such as their bank account number and routing number, and requests authorization to process single and recurring payments. They're particularly helpful for organizations that have subscription services, use set payment schedules, or want to improve their payment processing in areas such as:

- Cost savings: According to the National Automated Clearinghouse Association, the organization that oversees the development and administration of the ACH network, the median cost of processing ACH payments ranges between 15 and 25 cents, a fraction of what businesses spend on paper checks.

- Efficiency: With automated payments, SMBs that use recurring billing can save time and avoid chasing down customers for overdue balances.

- Enhanced security: Businesses and consumers can reverse ACH payments if they suspect fraud, and features like encryption make them far more secure than traditional checks.

- Reduced payment failures: Unlike credit cards, which frequently expire or change, bank account information typically remains the same, making it less likely that a recurring payment will fail to process.

Although these benefits are significant, they come with a few caveats. ACH payments process faster than paper checks, but they’re much slower than other types of digital payments. Businesses may have to wait a few business days to see a payment post, and ACH payments don't usually process on weekends or holidays, which can cause extended delays.

Furthermore, an ACH payment might receive initial approval, only for the business to learn later that it was rejected because the customer had insufficient funds. These kinds of failed payments sometimes result in fees, especially if an SMB experiences numerous returned payments.

Despite these challenges, ACH payments are ideal for eCommerce and serve as an enticing alternative for customers who don't want to use credit cards or paper checks, and the popularity of this payment technology continues to expand. In 2022, the number of ACH payments grew to 30 billion, totaling $72.62 trillion in transfers.

The difference between eChecks and ACH payments

Although eChecks and ACH payments are related, they aren't one and the same. The ACH is a network that allows for different payment types, and eChecks are one type of payment that can be processed over the ACH. In addition, whereas eChecks are often used for one-time payments, ACH payments are typically recurring. The processing fees for eChecks and ACH payments are also calculated differently in some cases.

Minimizing processing times with real-time payments

When looking to the future of electronic payments, eChecks, ACH payments, and payment gateways will remain mainstays. However, advancements in real-time payments (RTPs) have the potential to eclipse other payment technologies in terms of speed, convenience, and security.

The history of real-time payments

While credit card payments may take a day or two to process and eChecks might require a week or more, real-time payments (RTPs) are completed in a matter of seconds. This unprecedented processing speed is clearly described by the many names associated with them, including instant payments, faster payments, and immediate payments.

The first official RTP system, Zengin, began processing payments in Japan in 1973, but it took several decades for it to become available all day, every day. Switzerland's RTP system followed Japan's in 1987, yet widespread use of this payment type in the United States has only recently taken hold. The onset of the COVID-19 pandemic underscored the importance of updated payment processing technologies. As businesses shut down and employees were told to stay safe at home, paper checks and other types of payments sat in mail rooms, waiting to be processed.

Nevertheless, real-time payments in the United States remain far behind some other countries. For example, in 2021, India processed 48.6 billion real-time payments, compared to 1.8 billion in the United States. However, ACI Worldwide projects that this number will increase to 8.9 billion transactions by 2026.

The advantages and drawbacks of instant payments

RTPs have applications for many different types of businesses across multiple industries. For example, small retail businesses can instantly pay suppliers and service providers can collect funds from customers immediately after completing a job. Other advantages of RTPs include:

- Affordable rates: Advanced technology doesn't always equate to higher costs, and the processing fees for RTPs are usually similar to those for other payment methods.

- Constant availability: Some payments can only be processed during regular business hours, but RTP networks can process transactions every hour of every day, including holidays and weekends.

- Increased transparency: Consumers have a better awareness of their personal finances and businesses have stronger cash and liquidity management when transactions don't spend days or weeks trapped in processing.

- Faster payment reconciliation: When they can automatically reconcile payments, businesses can operate more efficiently, resolve errors more quickly, and reduce the likelihood of processing delays.

- Finality: Once a customer issues an instant payment, it can't be canceled or changed, helping to protect the interests and profits of SMBs.

These benefits promise great things for RTPs, but it's important for business owners to remember that they have some limitations. Because they process so quickly and are irrevocable, consumers and businesses have very little time to identify mistakes or instances of fraud. Security measures such as tokenization help reduce the risk, but greater fraud detection and prevention will help create a more secure and stable environment for RTPs in the coming years.

Available real-time payment networks

Unlike credit cards, checks, and ACH payments, which have well-established processing providers and networks in place, the infrastructure necessary for processing RTPs is still under development. In order to accept instant payments, businesses in the United States must be customers of banks associated with one of the two currently available RTP networks.

The Clearing House RTP Network

Until 2023, there was only one fully functioning network in operation in the United States: the Clearing House RTP Network. The network, which was launched in 2017, only provides RTP processing for businesses that are customers of banks affiliated with it. While some mobile payment apps, such as Zelle, offer instant transfer options using the Clearing House network, the implementation of RTPs in the American business world has been relatively limited in scope thus far.

FedNow

The Federal Reserve hopes to drive a rapid increase in the accessibility of RTPs with the launch of FedNow, a network that has been under development for many years. FedNow has now gone live and, like the Clearing House Network, allows participating banks and credit unions to complete instant transactions on behalf of their customers.

Because FedNow is a new network, only a few financial institutions have undergone the necessary testing and certification process. However, a greater number of SMBs will have the opportunity to use and accept instant payments as more banks seize the opportunity to join the network.

How SMBs can accept real-time payments

Business owners who decide that they want to participate in real-time payment transactions can begin by determining whether their institutions are connected to either the Clearing House or FedNow network. If they are, the next step is to make any needed changes to their merchant processing systems.

To achieve instantaneous processing, each RTP transaction must be processed individually rather than in batches. This involves a different setup than many SMBs have in place. By partnering with a technology provider, businesses can update their systems to accommodate RTPs and capitalize on an increasingly prevalent payment method.

Moving forward with electronic and real-time payments

When SMBs accept electronic payments, they improve their operational efficiency, cash flow, and customer experience. Unfortunately, the ever-growing number of payment options can prove overwhelming and confusing. Business leaders may wonder whether they have the time and resources to dedicate to learning about and deploying so many electronic payment technologies.

Whether a business wants to integrate a payment gateway into an online store or learn how to take advantage of the lightning speed of real-time payments, Sekure Payment Experts is happy to help. The Payment Experts at Sekure specialize in credit card payment services, assisting businesses with every aspect of their payment processing needs, from getting the lowest possible rates to exploring the pros and cons of various payment gateway integrations. Sekure's team of Payment Experts can also empower you to achieve fast funding with fast deposit solutions, so you always have your money when you need it.